It’s important to have an investment philosophy – an approach to guide your decisions and ground you during market turmoil – that you can stick to long-term. The discipline to remain committed to your plan means as much as the plan itself. Many different approaches can work given enough time and commitment. What doesn’t work is the absence of a plan, or jumping from one to another at the first bit of uncertainty.

Recently, there’s been chatter that your investment approach should be based on cheap index funds since active managers cannot outperform, and paying for hope is wasted money. Data support the chatter. Active managers haven’t done well.

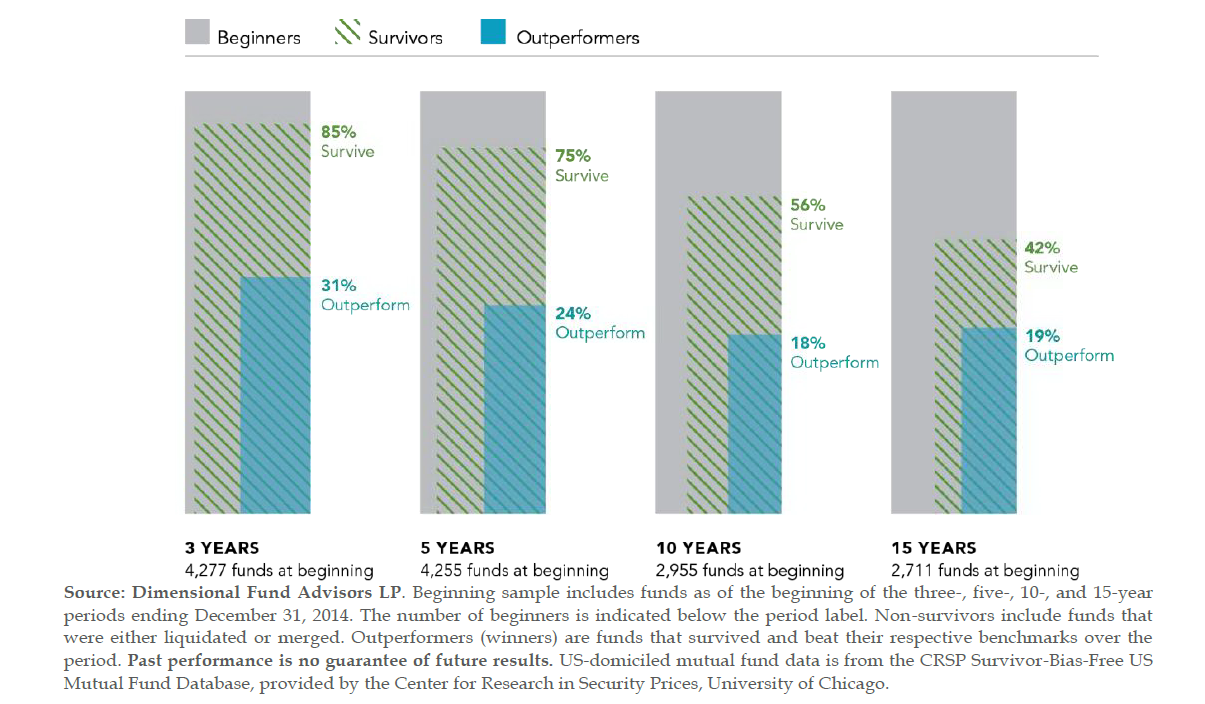

Survivorship and Outperformance

Performance periods ending December 31, 2014 — Equity Funds

For the five, ten, and fifteen year time periods shown above a mutual fund had better odds of going out of business than outperforming, and the overwhelming majority underperformed. Myriad theories exist about why, but theories only matter in ivory towers and conference rooms. They contain great phrases like paradox of skill, efficient markets, active share, benchmark hugging, etc., but you’re trying to figure out how to invest. We can save the theories for later.

Many investors have centered in on one primary reason for underperformance –active managers cost more and fees are a performance drag that cannot be overcome. Once again, the numbers don’t lie.

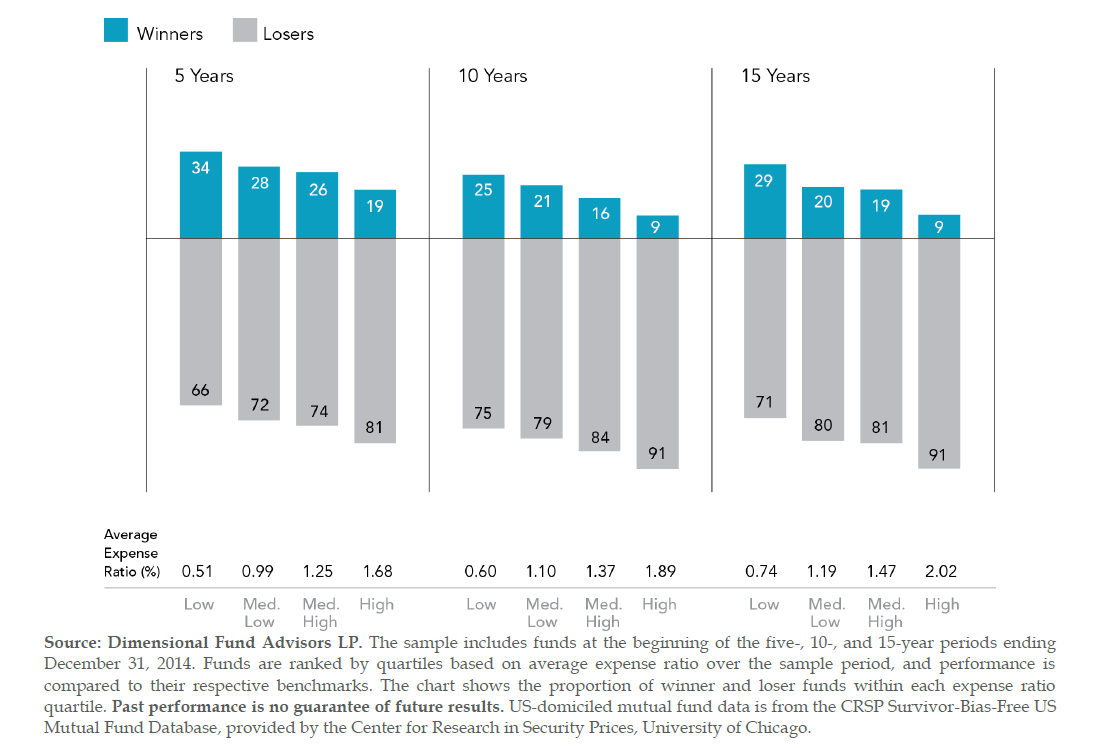

High Costs Make Outperformance Difficult

Winners and losers based on expense ratios (%) — Equity Funds

The lower the fee, the better chance you have to outperform, and vice versa. Some investors have pushed this to its logical extent and plowed money into index funds. If outperformance is difficult, and paying less means earning more, it’s a rational response.

Yet, for some reason it leaves me lacking, and not because I have some career conflicting aversion to it. Our firm could use index funds for our clients if we believed in them. Don’t get me wrong, there are things I like about index funds. Lower-fee and lower-turnover approaches make sense. Our firm uses strategies that meet these criteria as well. We show the advantage of lower fees above. Lower turnover funds that keep costs down by placing fewer trades and are more tax-efficient help investors keep more of what they earn.

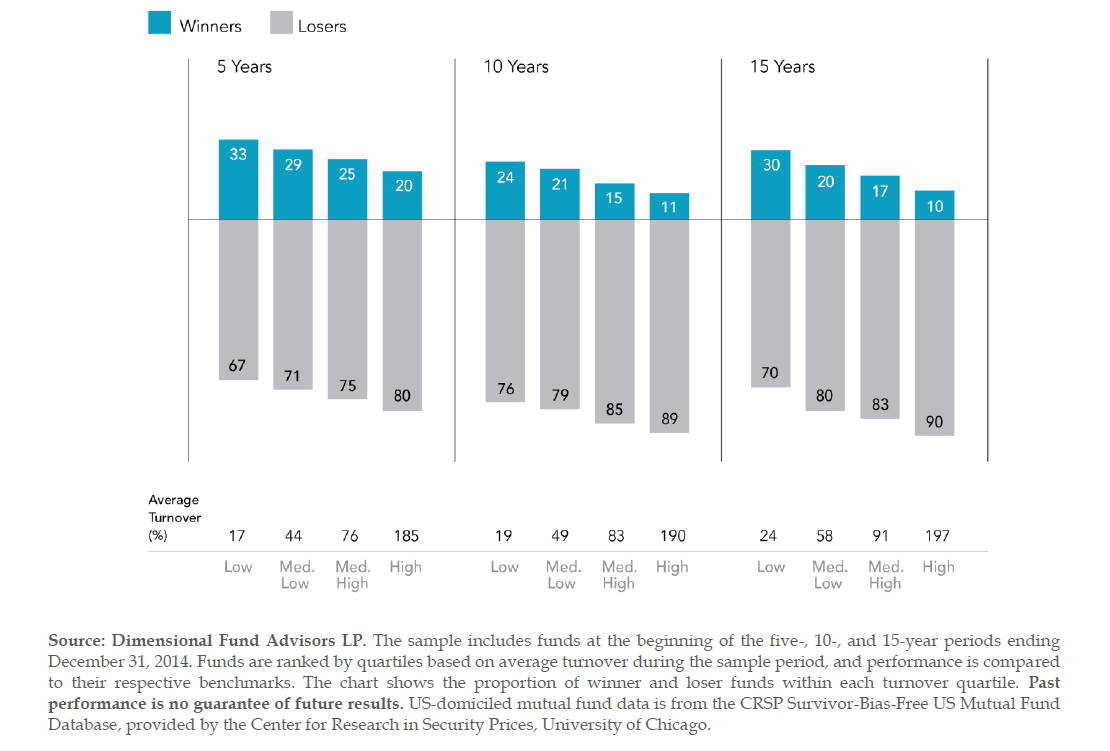

High Trading Costs Make Outperformance Difficult

Winners and losers based on turnover (%) — Equity Funds

However, boiling investments down to one variable, fees, doesn’t make enough sense to me. There are things about indexing I don’t like. The biggest one is that the index doesn’t care about price.

I’m price conscious in everything I do. People call me cheap but I prefer to say I appreciate value. I’ve been conditioned to believe (and handle my financial life accordingly) that what you pay for something matters. I just can’t love an investment approach that forces me to own more of what’s expensive and less of the cheaper stuff.

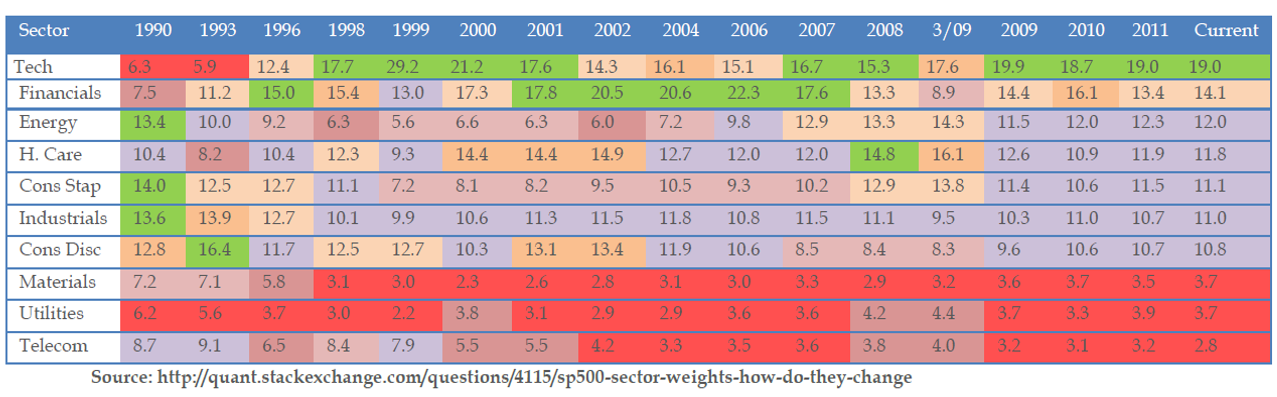

How excited would you be to invest with a manager that had 29.2% of its portfolio in technology stocks to end 1999 right before the bubble in technology stocks burst? What if that same manager had only 6.3% of its portfolio in energy stocks when oil prices had bottomed out at $16.42 before climbing to a peak of $144.78 in 2008? And what if that manager had 22.3% invested in financials before the 2007 crash? Well, that’s what an S&P 500 index fund did.

Historical Sector weightings of the S&P 500: 1900–Current

Indexing is fine until it isn’t. When the market tumbles, it tends to tumble from the top down, meaning the most expensive sectors or stocks feel more than their fair share of the market decline. The technology sector by 2002 had gone from 29.2% (in 1999) of the S&P 500 to 14.3%. Financials had moved from 22.3% in 2006 to 8.9% at the market bottom in March, 2009.

I’d prefer to factor price into my investment decisions to avoid concentrating my portfolio in expensive sectors and buy cheaper ones. I’d also like to do it in a way that still retains some of the advantages of indexing (low fees, lower turnover, and tax-efficiency), so I can keep more of what I earn from the markets.

That’s what our firm is looking to do in our portfolios. A low-cost investment experience that factors in price, still has lower fees and portfolio turnover, and does a few other things that make sense for our clients which gives them a reasonable opportunity to extract maximum performance from the markets. Rather than blindly buying an index (or a set of indices) and de-linking our client portfolios from any definition of value, our firm prefers to have our clients’ stock allocations be exposed to certain things that have rewarded investors over time.

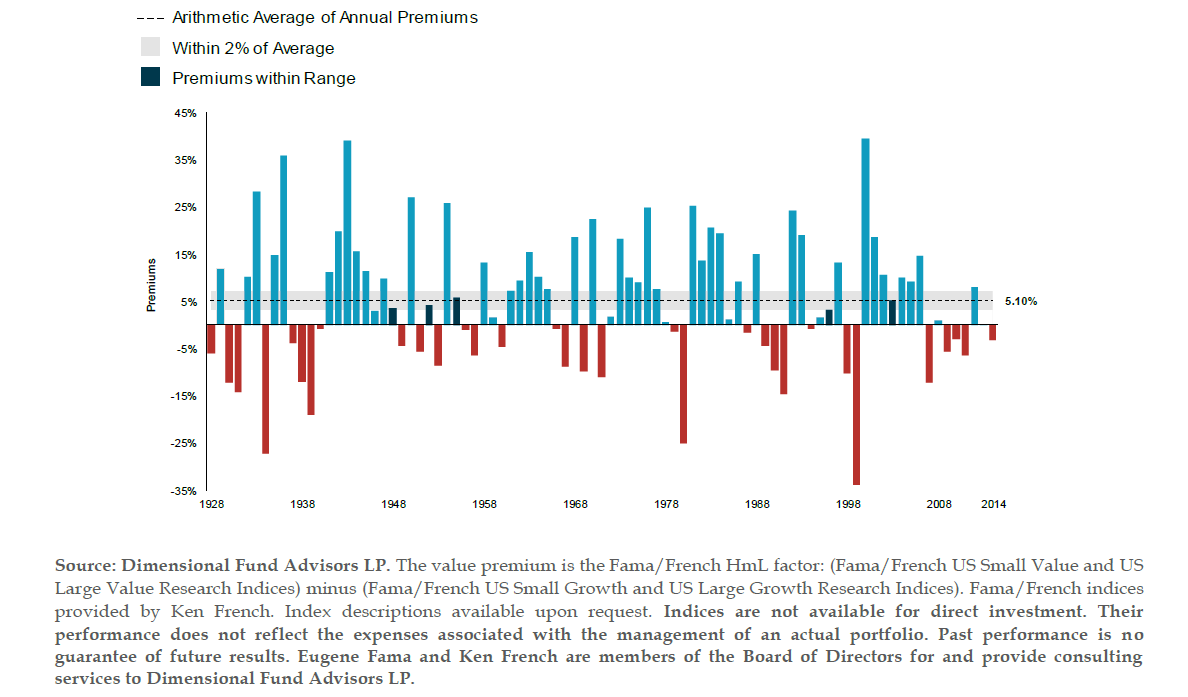

The first is value. Historically, value stocks have outperformed growth stocks by an average of 5.10% between 1928 and 2014. This outperformance does not come every year, but has been available to the long-term investor.

Value minus growth: US markets 1928–2014

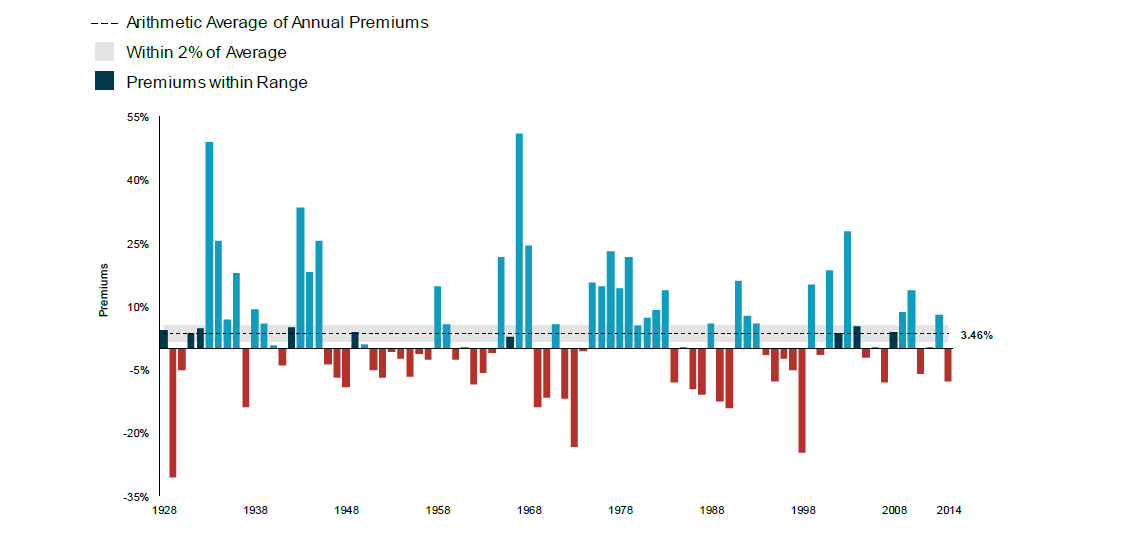

Second, investors have been rewarded for investing in smaller companies.

small cap minus large cap: US markets 1928–2014

Our firm currently has a higher allocation to small cap stocks in its clients’ portfolios than the market indices to try and take advantage of that 3.46% outperformance.

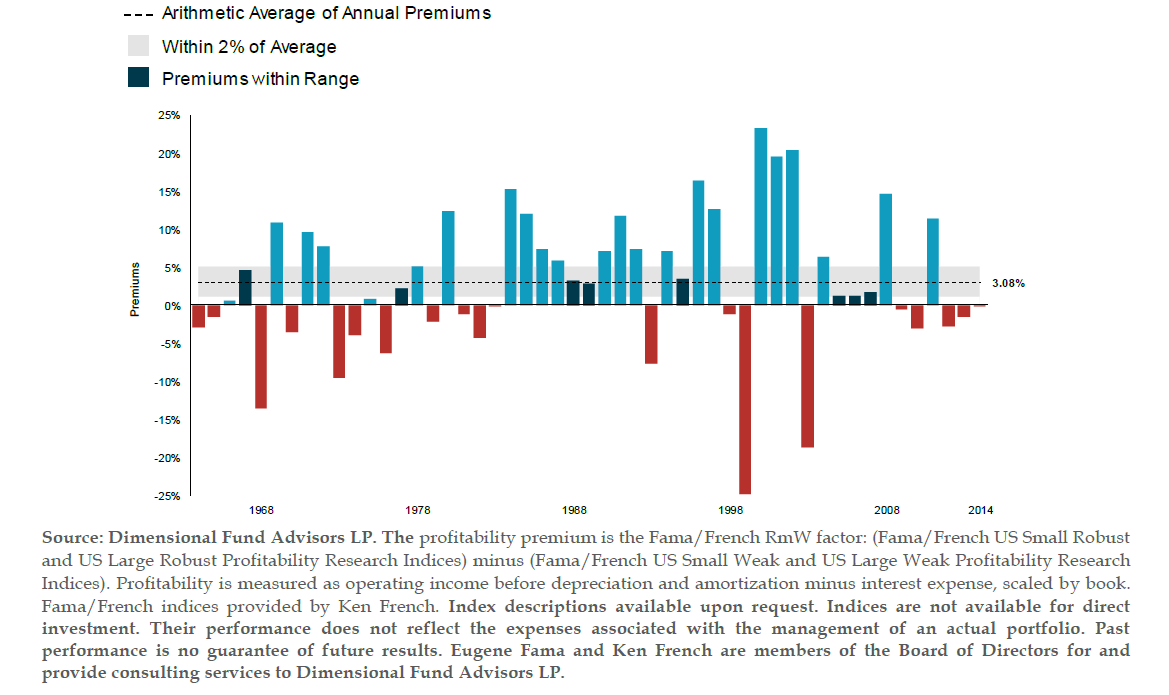

Third, profitable companies have historically outperformed less profitable ones.

High profitability minus low profitability: US markets 1964–2014

Focusing on (1) cheaper stocks, (2) smaller companies and (3) profitable companies makes a lot of sense to me, somewhat of a no-brainer perhaps. However, indexing doesn’t do that for you. Indexes are typically market cap weighted, which means that the bigger the company, the more you own. In addition, the stronger the performance of the stock, the more you own. Instead of building stock portfolios around one variable, our firm takes a more balanced approach. We use low cost funds that have low turnover, but expect our managers not to ignore common sense pricing and structural advantages that could help our clients in the globally diversified portfolios we build for them.

How much we invest in stocks is based on our clients’ financial plans and the current market environment. Historically, stocks have outperformed other asset classes, and we want to expose clients to stocks to the extent we can, given their long-term goals and current valuations. However, this stronger return potential comes with significantly higher short-term volatility and risk of short-term loss, so clients usually need to own other asset classes. The exact allocation to those classes depends on their time horizon, withdrawal needs, and investment environment. For stability and income we usually add bonds, whose quality and duration depends on our views of the bond market at the time. Similar to our stock investing, we focus on price and risk/reward in the current investment climate.

Fixed Income

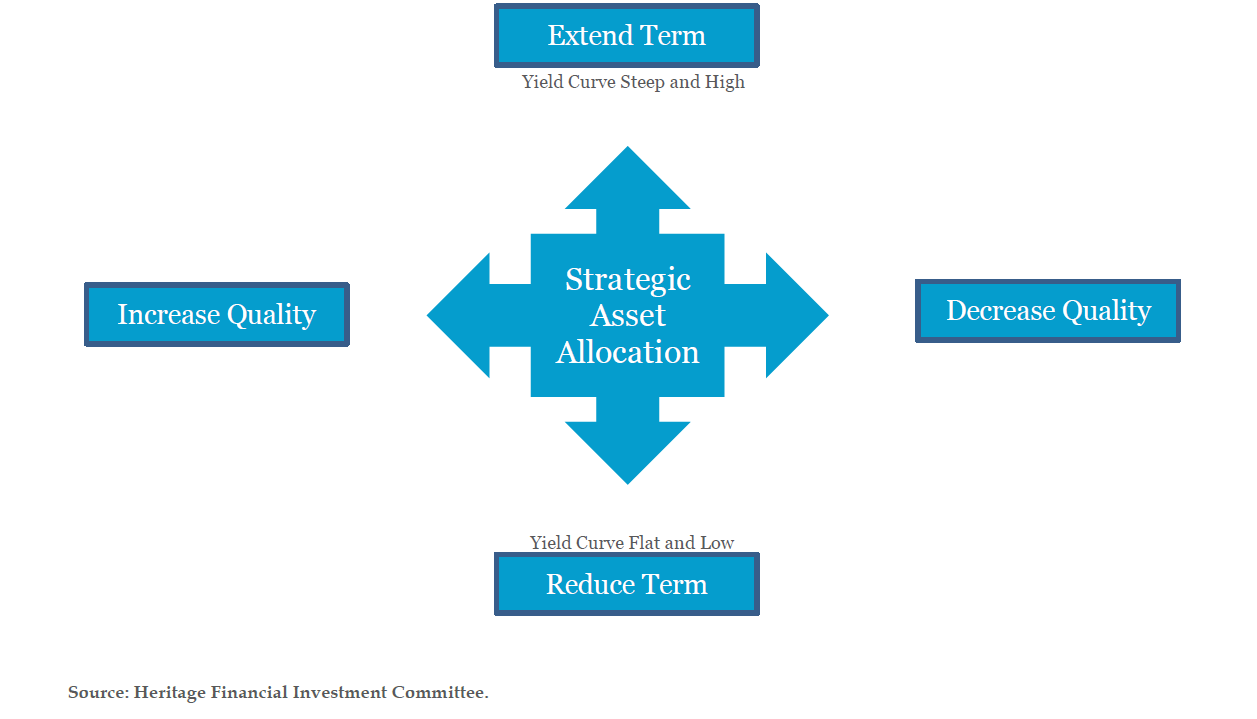

Selecting Risk Profile in the Fixed Income Market

Our firm prefers to invest in lower quality bonds when credit spreads widen and investors are paid to own them. We can then increase quality when we are not being paid to take the risk. Similarly, we prefer to own longer-term bonds when the yield curve is steep and we expect to be compensated for the duration risk. We prefer to own shorter-term bonds in the opposite scenario.

For diversification and a different source of positive return, our firm will complement these two asset classes with alternative investments that meet the following criteria:

1. A positive expected long-term return relative to the stocks and bonds used to fund them

2. Investments that shouldn’t move in tandem with the stock and bond markets or each other so they are providing portfolio diversification and risk management

In sum, I believe focusing on fees is appropriate, but limiting your investment philosophy to just one variable doesn’t make enough sense when it forces you to ignore price discovery and the fundamentals that could lead to a higher return. You need to have a framework for investing in bonds since they can provide stability and protection during market declines. Select alternative investments may add value in the right situations. The exact mix of how much you have in all three (your asset allocation) should be guided by your financial plan and personal situation. A professional advisor can help with all of these steps and more, but it’s important that their investment philosophy resonates with you so you can stick to it long-term.