Key Observations

- Markets Warm with the Weather – May brought a more constructive tone as trade tensions eased, lifting sentiment and encouraging a rebound in risk assets.

- Fixed Income Buyers Remain Cold – While equities priced in potential fiscal stimulus, bond markets focused on long-term deficit risks, pushing yields higher across most of the yield curve.

- Fed Independence Under the Spotlight – The Fed has held rates steady this year while calls from the Executive Branch grow louder to ease policy. Investors wonder yet again how independent the Fed truly remains.

- Fed Structure Limits Political Control – Fed governors serve staggered 14-year terms and require Senate confirmation, but average tenure is only about seven years. While this structure gives presidents some influence, it falls short of control. This is especially true given that the full voting Federal Open Market Committee (FOMC) includes five regional presidents unaffiliated with the Executive Branch.

- Imperfect Independence – Despite renewed debate around Fed leadership and independence, there is no current evidence to suggest investors should shift positioning. The Fed remains an imperfect yet vital anchor for monetary stability.

Market Recap

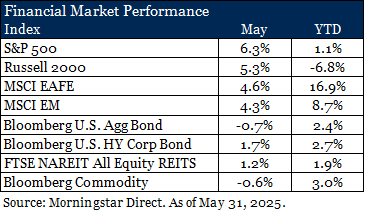

May brought a welcome change in tone, both in the weather and the markets, as the warmth of spring settled across North America. The initial jolt from April’s tariff announcements faded into more tempered discussions and signs of de-escalation. Investors responded in kind, especially in the growth-oriented corners of the market.

Technology stocks, once again led by the “Magnificent Seven,” surged ahead. In May, the sector climbed an impressive +10.9%, making it the only sector to notch double-digit gains and distinguishing it as the clear winner of the month.

Not all sectors shared in the rally. Healthcare, in contrast, struggled under the weight of renewed political scrutiny. Concerns over drug pricing rhetoric and uncertainties tied to pending tax legislation dragged the sector down -5.5%, making it the only U.S. sector to post a decline for the month.

Optimism was most concentrated in U.S. markets which helped them pull ahead of their international peers. The S&P 500 outpaced the MSCI EAFE and MSCI EM by +1.72% and +2.03%, respectively, for the month. Still, allocations outside the U.S. remain in the lead year-to-date, bolstered by solid local market returns and a weak U.S. dollar year-to-date.

Not all investors were comforted by the easing of trade tensions. Bond markets responded more cautiously. While equities leaned into the possibility of new fiscal stimulus, fixed income investors focused on the long-term implications for the federal deficit. Yields rose across most of the curve, except at the short end, as the Federal Reserve kept rates unchanged and signaled its ongoing inflation vigilance. The backdrop for bondholders remains complex, shaped by policy uncertainty, legal challenges to tariff plans and the broader fiscal outlook.

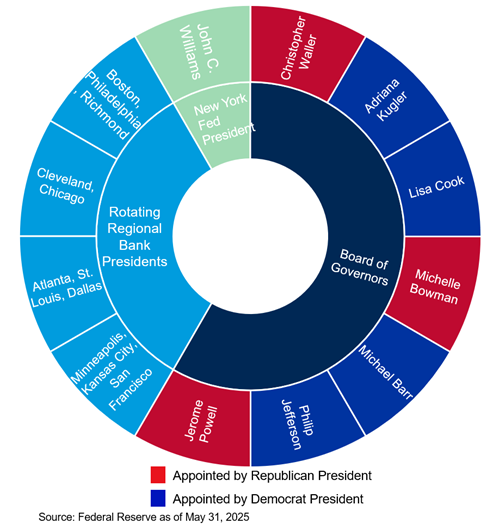

To that end, May marked the one-year countdown for Federal Reserve Chair Jerome Powell’s term as chair, which will end in 2026. While his seat on the Board of Governors ends in 2028, the question of leadership, and by extension Fed independence, is back in the spotlight. Add to this the open interest from President Trump for lower rates and investors are again asking: how insulated is the Fed from political pressure, really?

What’s At Stake?

Fed independence is not about optics or tradition. It is foundational to stable prices and economic growth. When it falters, the fallout is real. History shows us that political interference in monetary policy can fuel inflation, destabilize asset prices and increase the cost of capital. The risk is not a theoretical concern; it is existential for allocators. If investors lose confidence in the Fed’s impartiality, global demand for U.S. Treasuries could soften and the margin of safety that underpins valuations across all asset classes, from growth stocks to municipal bonds, could erode.

Fed Structure

The Fed is designed to resist political overreach. The seven-member Board of Governors serve staggered 14-year terms, and appointments require Senate confirmation. At face value, this would indicate very modest influence in any one term for a sitting President. However, only about 17% of governors serve out their full term, with the average tenure being seven years since 19141. This built-in turnover gives sitting Presidents the potential for more influence, but far short of control. Even with board turnover (which is no guarantee) and the existence of term limits, history suggests that appointing more than four governors in a single presidential term would be highly unusual. Moreover, the appointed board is not the full committee.

The 12-member Federal Open Market Committee (FOMC) includes five regional Fed presidents who are not appointed by the White House. Seven votes are needed for a majority. The regional presidents serve as a structural buffer, mitigating the potential for appointee influence.

Independent, Not Infallible

There are notable historical examples of the Fed’s wavering independence. In the 1940s, the Fed suppressed interest rates to help finance war spending. The Fed voluntarily acted to do so in such an extraordinary time, but clearly this policy extended beyond purely economic intent. Inflation surged post-war until the breaking point came in 1951 when the Treasury-Fed Accord freed the Fed from rate pegs. This act is now regarded by some as the true birth of modern monetary independence.

Chair Arthur Burns yielded to political pressure to cut rates in the 1970s, a move that when combined with other macro factors contributed to runaway inflation. Conversely, Paul Volcker’s resolve in the face of political threats during the 1980s exemplified why independence matters. Although his rate hikes were painful, they restored credibility and anchored long-term inflation expectations, leaving a lasting impact to this day.

Legal Precedent

The 1935 Supreme Court case Humphrey’s Executor established that independent agency heads cannot be removed by the President without cause. While not Fed-specific, the ruling underpins the legal architecture protecting the Fed’s autonomy. That does not mean political will won’t try to test it, but it does mean any attempt at structural overreach would face steep legal hurdles.

Outlook

The Fed is not infallible, but its design and legal safeguards meaningfully limit short-term political influence. That is not just a procedural win; it offers a structural advantage for long-term investors. Economic policy that bends to election cycles tends to deliver short-lived gains and long-term consequences.

As the market begins to price in potential leadership transitions and shifting policy postures, long-term allocators would do well to focus elsewhere. Structural drivers like fiscal policy, entitlement spending and the trajectory of U.S. deficits are far more likely to influence Treasury yields and capital markets than the next one or two Fed appointments.

Fed independence deserves attention, especially when headlines blur the lines between politics and policy. But perspective matters: history and institutional design suggest that the Fed remains an imperfect but resilient anchor of monetary stability. For now, we see no evidence that warrants a change in positioning based on this issue alone.

Listen and subscribe to our Wealthy Behavior podcast to stay up-to-date on the latest market, economic and investment news that affects your wealth. If you like what you hear, please leave our show a review on Apple Podcasts or Spotify so we can reach more people like you!

[1]Federal Reserve from August 10, 1914 to March 1, 2025