Disruption from AI paves way for assets outside of U.S. large cap.

Key Observations

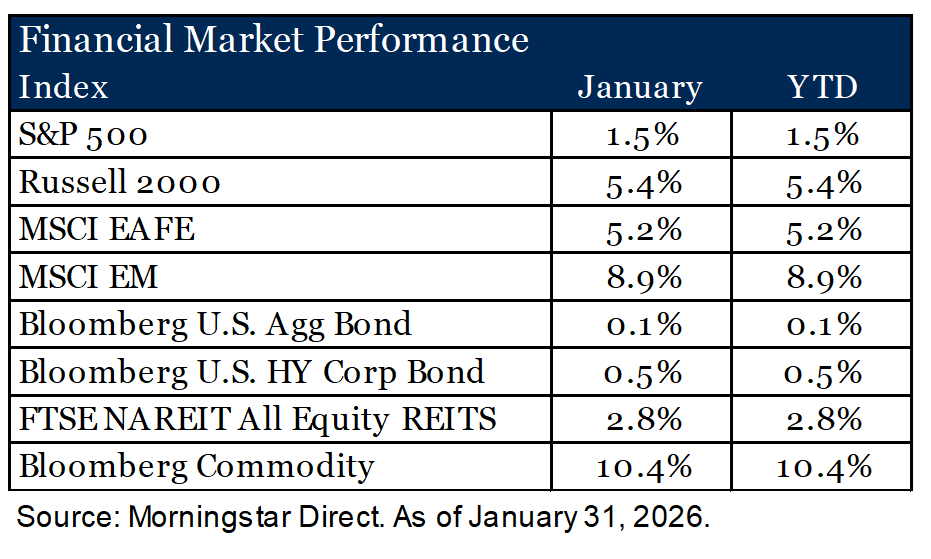

- Global markets started the year strong and were broadly positive across asset classes in January.

- Concerns of potential disruption from new AI tools wreaked havoc on select sub-sectors such as software. Areas such as U.S. small cap and emerging market equities benefited from a rotation away from U.S. large cap.

- President Trump nominated Kevin Warsh to be the 17th chair of the Federal Reserve. Markets initially viewed this as “hawkish” but his views on inflation and productivity could lay the groundwork for more rate cuts.

Market Recap

January opened the year with a more confident tone across global markets. Markets were focused on the path of monetary policy, early corporate earnings signals and geopolitical developments that shaped sentiment throughout the month. Equity markets generally advanced and commodity markets rallied sharply. The combination created a constructive backdrop that helped most major asset classes deliver positive returns to start the year.

Large-cap U.S. equities posted a modest opening month. The S&P 500 Index gained 1.5%, supported by pockets of strength in energy and communication services, along with steady demand for higher quality large cap companies within consumer staples. Small cap stocks performed even better as concerns grew about the impact generative AI might have on software-related companies and investors rotated into more attractively valued areas of the market. The Russell 2000 Index rose 5.4% in January. Softer inflation, improving business surveys and an overall economic backdrop that remains resilient helped fuel the asset class.

International developed equities outpaced U.S. large caps. The MSCI EAFE Index advanced 5.2%, helped by broad strength across Europe and Japan. European equities found support from central bank communication that pointed to stable policy in the near term, while inflation remains moderate. Japanese equities rose as well.

Investor concerns surrounding geopolitical tensions in the Middle East and Eastern Europe remained present but did not dampen the regional rally. A weakening U.S. dollar further helped the space. Emerging markets delivered the strongest equity performance in January. The MSCI EM Index climbed 8.9%, led by strong gains in South Korea, Mexico and Brazil. Technology shares in Asia rebounded sharply, supported by improving semiconductor demand and favorable trade expectations tied to early conversations about reopening supply channels between major economies. Latin America benefited from resurgent commodity demand and further currencies.

Fixed income markets generated modest gains as interest rate volatility remained. The Bloomberg U.S. Aggregate Bond Index returned 0.1% for the month. Treasury yields moved modestly higher during the period as the expectation for the number of rate cuts in 2026 diminished and the markets digested the announcement of Kevin Warsh as the next Fed Chair nominee. Credit markets extended the positive tone. High yield bonds, measured by the Bloomberg U.S. Corporate High Yield Index, rose 0.5%, supported by narrowing spreads, resilient corporate fundamentals and a favorable economic backdrop.

Diversifying areas of the markets such as REITs and commodities also opened the year in positive territory. U.S. Equity REITs gained 2.8% during January. The sector benefited from early signs of improving fundamentals in data centers, industrial properties and select residential markets. Concerns around office properties persisted, but strength in other areas outweighed the drag. Commodities delivered the most notable performance of the month. The Bloomberg Commodity Index surged 10.4%, driven by strength in energy and industrial metals. Energy prices, particularly crude oil and natural gas, moved higher as extremely cold temperatures swept across much of the country. Precious metals saw favorable returns as well, although gold prices sold off at the end of the month, limiting the gains.

Mixed Impact from AI

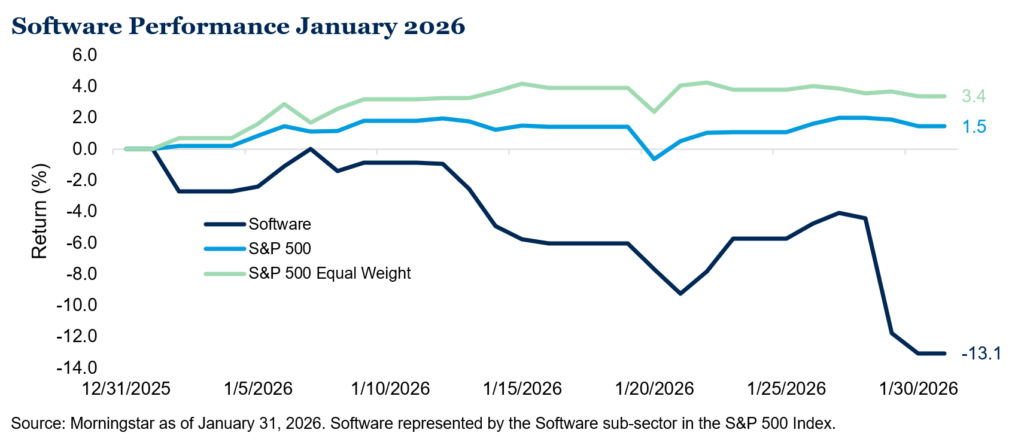

January brought mixed impact from AI during the month. We discussed the potential for disruption and displacement from AI as part of our “AI Playbook” theme in our 2026 Outlook. Investor concerns took hold about the potential disruption generative AI would have on software companies during the month following a new tool for Anthropic’s Claude large language model that can help with tasks for legal, marketing and data analysis. Shares of Oracle and Salesforce fell over 15% and 19%, respectively, for the month and resulted in the software sector being down 13.1%, wiping out nearly $800 billion in market value.1 On the other hand, semiconductor companies, particularly abroad, continue to benefit from the demand for chips and flash memory. We highlighted in our Outlook that having thoughtful diversification to areas of the market such as non-U.S. equity and small and mid-cap U.S. stocks may help balance portfolios and capture the benefits from a broadening of AI, and we are seeing this take shape so far in 2026.

A New Fed Chair Nominated

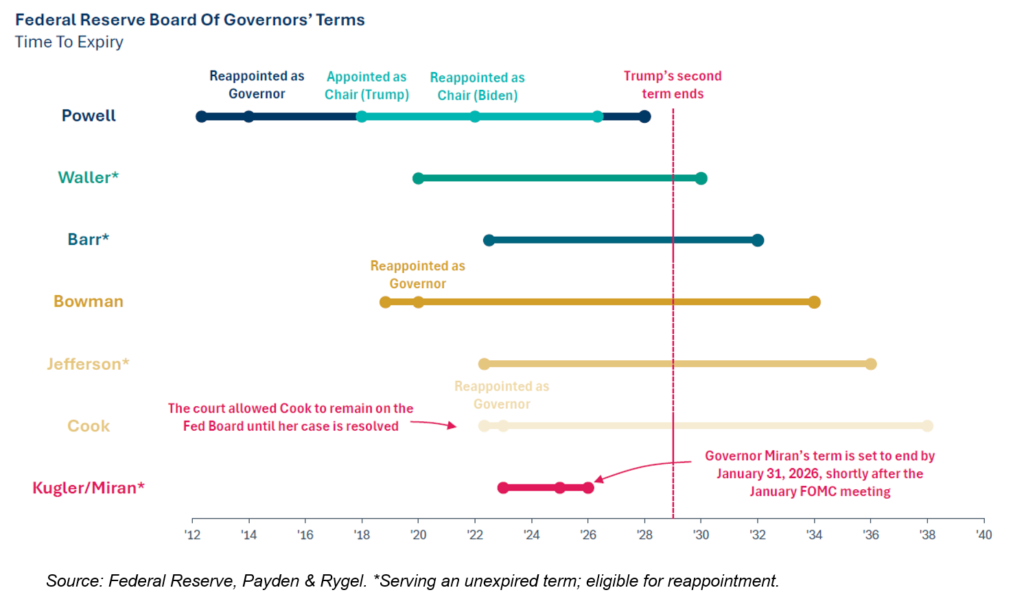

After weeks of the markets speculating, President Trump announced the nomination of Kevin Warsh to be the 17th chair of the Federal Reserve. If confirmed by the Senate, Warsh would take the lead seat in mid-May when Powell’s term as chair ends. It is important to note that Powell’s term on the board of governors does not end until 2028, unless he voluntarily steps down, and that Warsh would be replacing Stephen Miran. The market initially reacted viewing Warsh as a “hawk” based on his past Fed governor experience and his comments on balance sheet reduction. Interest rates ended the month modestly higher from where they began at the end of last year and the price of gold fell over 7% on the day of the nomination.2 But Warsh’s views on current productivity could help lay the groundwork for future rate cuts.

The nomination brought the topic of Federal Reserve independence once again to the forefront of investor concerns, something that has been ongoing over the past 18 months. It is important to note this is not the first time in history that the subject has been discussed. In fact, Warsh, who served as a Fed Governor from 2006 to 2011, addressed the issue in a 2010 speech in New York: “Independence in the conduct of monetary policy is at the core of advanced modern economies. And it can be too easily forgotten by those who have only known its benefits.

“If the Federal Reserve lost its independence, its hard-earned credibility would quickly dissipate.”

-Kevin Warsh, 2010

If the Federal Reserve lost its independence, its hard-earned credibility would quickly dissipate. The costs to the economy would be incalculable: Higher inflation, lower standards of living, and a currency that risks losing its reserve status.”3 We discussed the FOMC structure in depth in our May Market Review last year, Imperfect Independence. Our stance remains the same, that the institutional design should minimize short-term political influence and based on the current terms, the current administration has limited ability to appoint new governors assuming terms are served in full.

Outlook

Overall, January provided a constructive start to the year across global markets. Many of our themes from our 2026 Outlook are taking shape. Diversifying positions away from U.S. large cap have been beneficial to start the year (small-cap U.S. equities and non-U.S. equities in particular). A resilient economy and strong corporate fundamentals are supportive for markets, but we remain mindful of current valuations, market concentration and the uncertainty created by geopolitical events.

Listen and subscribe to our Wealthy Behavior podcast to stay up-to-date on the latest market, economic and investment news that affects your wealth.

If you like what you hear, please leave our show a review on Apple Podcasts or Spotify so we can reach more people like you!

1. FactSet. As of January 31, 2026. Market value based on the software sub-sector of the S&P 500 Index.

2. FactSet. As of January 30, 2026

3. Federal Reserve. Speech by Kevin Warsh March 26, 2010. https://www.federalreserve.gov/newsevents/speech/warsh20100326a.htm