Key Observations

• Markets repriced in April on “higher-for-longer” rates pushing longer duration fixed income and duration sensitive equities lower. Small-cap growth stocks were hit as the two largest securities in the index declined -15% and -37% due to moderating AI spending concerns.

• Escalating conflicts in the Middle East have led investors to question what impact expanded conflict may have on their portfolios. Increasing oil prices has modestly priced in risk of expanded conflict into neighboring petrostates Iran and Israel.

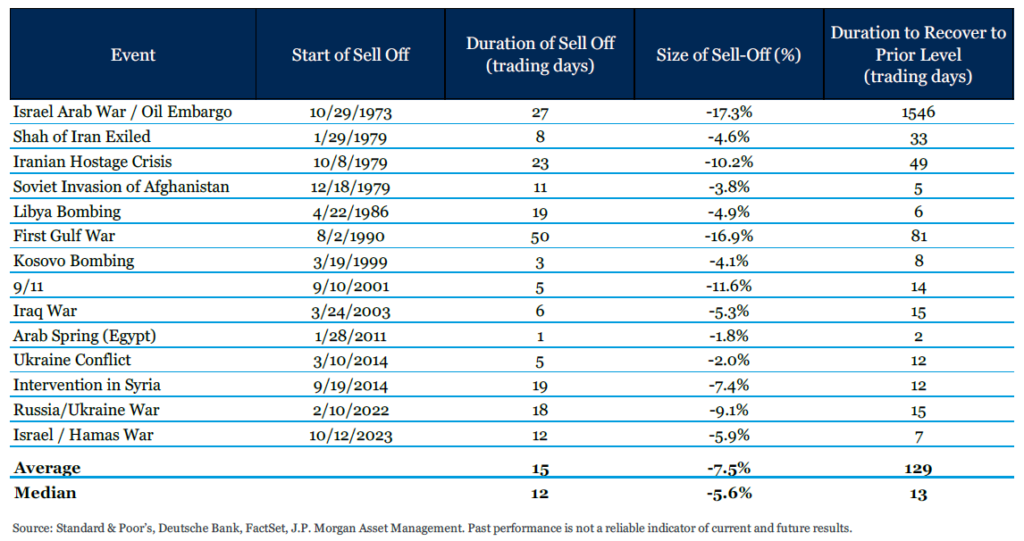

• While these events capture our attention, their fundamental impact on markets tends to be short-lived. With history as precedent, both the duration of a market downturn and the subsequent recovery from such events are typically measured in days rather than months or years.

Market Recap

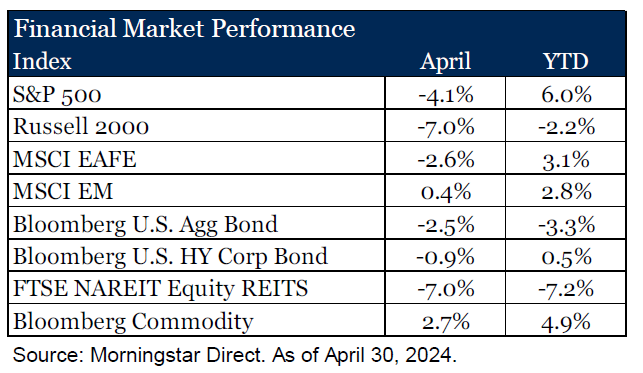

The S&P 500 Index departed from its five-month ascent, recording a -4.1% decline. Despite the advance estimate of 1.6% 1Q 2024 GDP growth reported in April, concerns arose as the pace of expansion decelerated from previous quarters, marking a departure from the six consecutive quarters of growth exceeding 2% according to BEA data.

Inflationary pressures persisted as the core Personal Consumption Expenditures (PCE) deflator of 2.8% remained above the Federal Reserve’s long-term target of 2%, marking a modest acceleration from previous reports. This upward trend challenged interest rate cut expectations and fueled speculation of a prolonged period of higher rates.

With expectations of a stable rate policy in the U.S. and the possibility of rate cuts from other central banks, the resilience of the U.S. dollar continued, marking its fourth consecutive monthly gain, the longest streak since September 2022.

The shift in rate expectations rippled across markets, causing repricing of many assets. In fixed income, longer-duration assets underperformed shorter-duration ones as rates rose. In U.S. equity markets, strength was observed in energy and utilities, which tend to be less sensitive to interest rates, while more traditional growth sectors retreated. Small-cap stocks faced similar, but more acute, headwinds, with the two largest securities (Super Micro Computer and Microstrategy Inc) in the index declining -15% and -37% due to moderating AI-driven spending. This pushed the Russell 2000 Index down -7% for the month.

Despite the strength of the dollar, international markets forged ahead for the month. MSCI EAFE outperformed the U.S. and was supported by the continued rally in Japanese stocks. MSCI Emerging Markets witnessed a resurgence, buoyed by China’s performance after enduring a period of underperformance earlier in the year. This positive turn provided a glimmer of optimism amidst global economic uncertainties and trade dynamics.

Expansion of Conflict in the Middle East

We witnessed a direct escalation of conflicts in the Middle East during the month, which stemmed from a retaliatory strike on Israel by Iran, which had been anticipated. While these two nations have been engaged in a shadow conflict for decades, this recent escalation has prompted investors to consider the potential impact of a broader conflict on their portfolios. Below we explore the nature of military conflict and its implications for our investment principles and outlook.

First, let us discuss principles. Military conflicts, much like other external events such as natural disasters, are challenging to integrate into investment strategies. By their very nature, they often arise suddenly and with considerable uncertainty. The inevitability of events with timing that is often unknowable, and their uncertain impact on prices, underscores a fundamental principle of investing: diversification. Diversification acknowledges the reality of imperfect information. With perfect information we would invest solely in the highest-returning asset and disregard all others. However, because we can’t predict outcomes with certainty, thoughtful diversification, without overdoing it, helps establish resilience in the face of unpredictability.

Regarding our outlook, explicitly incorporating conflicts into our assessments is difficult at best. While we cannot afford to ignore them, we also cannot precisely “price” them in allocations. Instead, the possibility of such events becomes part of a broader risk management framework. Given the nature and geographic location of the escalating conflict between Israel and Iran, risk management shifts focus to unexpected inflation, particularly through higher oil prices.

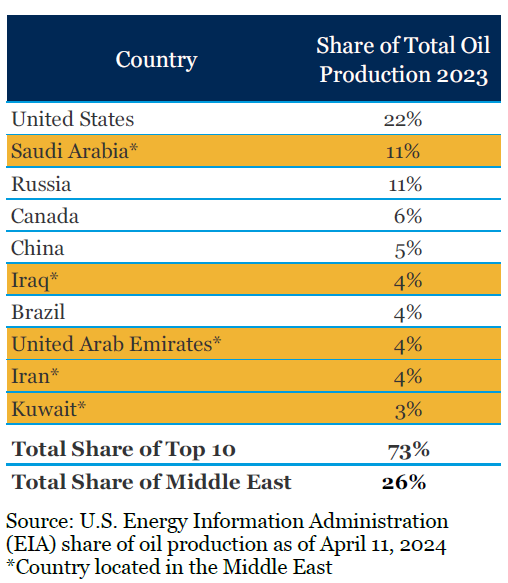

Oil prices initially surged after the outbreak of renewed conflict in the Middle East last October. Although they briefly retreated from their initial rally, oil prices have been steadily climbing this year. The rise in prices is attributed to the conflict expanding into neighboring petrostates such as Iran and Saudi Arabia. Iran’s oil production accounted for 4% of global supply in 2023, while Saudi Arabia, the region’s largest producer, stands at 11%. Markets are sensitive to potential disruptions in supply, especially in a tight oil market with Russian sanctions. Additionally, the U.S. is the largest swing producer and is already near peak volumes. Energy prices are a crucial factor influencing inflation and continue to draw the attention of investors as they await the Fed’s stance on rate cuts. Furthermore, disruptions in the Middle East could exacerbate inflationary pressures by constraining shipping via the Red Sea and/or the Suez Canal. Such events are a reminder of one of the reasons we own real assets in our diversified portfolios. Exposure to the asset class is often of notable value in periods of unexpected inflation.

Oil prices initially surged after the outbreak of renewed conflict in the Middle East last October. Although they briefly retreated from their initial rally, oil prices have been steadily climbing this year. The rise in prices is attributed to the conflict expanding into neighboring petrostates such as Iran and Saudi Arabia. Iran’s oil production accounted for 4% of global supply in 2023, while Saudi Arabia, the region’s largest producer, stands at 11%. Markets are sensitive to potential disruptions in supply, especially in a tight oil market with Russian sanctions. Additionally, the U.S. is the largest swing producer and is already near peak volumes. Energy prices are a crucial factor influencing inflation and continue to draw the attention of investors as they await the Fed’s stance on rate cuts. Furthermore, disruptions in the Middle East could exacerbate inflationary pressures by constraining shipping via the Red Sea and/or the Suez Canal. Such events are a reminder of one of the reasons we own real assets in our diversified portfolios. Exposure to the asset class is often of notable value in periods of unexpected inflation.

Ultimately, while these events capture our attention, their fundamental impact on markets tends to be short-lived. With past as precedent, both the duration of a market downturn and the subsequent recovery from such events are typically measured in days rather than months or years.

Listen and subscribe to our Wealthy Behavior podcast to stay up-to-date on the latest on the market, economic and investment news that affects your wealth. If you like what you hear, please leave our show a review on Apple Podcasts or Spotify so we can reach more people like you!