February Market Recap

Warm winter weather seems to have been fueled by hot January economic data reported in February. Employment, retail sales, manufacturing, and inflation all showed acceleration. Markets fell in sympathy. Why? The irony of positive economic surprises is markets interpret that as the Fed has more rate hikes ahead. We’ll unpack more of the details below.

For the month, markets broadly were down across most major asset classes. Domestic markets, particularly growth, held up based on the rally in semi-conductors and China pulled down ex-U.S. markets following its extraordinary rally from October of last year. Malaise around U.S. – China relations and an attempt to gauge the degree to which Chinese consumers will emerge from COVID lockdowns has some investors taking profits.

Markets Swallow Upside Surprise on Economic Data Whole

February brought on a rush of positive economic data. Unemployment fell to 3.4% (the lowest since 1969) coupled with a blockbuster 517,000 jobs added in January*. Personal income grew 0.6% in January coupled with retail sales showing a very strong January growth of 3%. Strong employment and spending figures translated to inflation accelerating in January up 0.5% compared to a more temperate increase of 0.1% in December*. Our take, while good news, is there may be some noise in these figures that may make them rosier than they appear. For example, seasonal layoffs did not occur nearly to the same degree as they have in the past based on the struggles of businesses to fill open positions, so employment surprised to the upside. Or perhaps the 8.7% cost-of-living adjustment for Social Security and/or the drop in in consumer savings rates may have boosted spending in an unsustainable way.

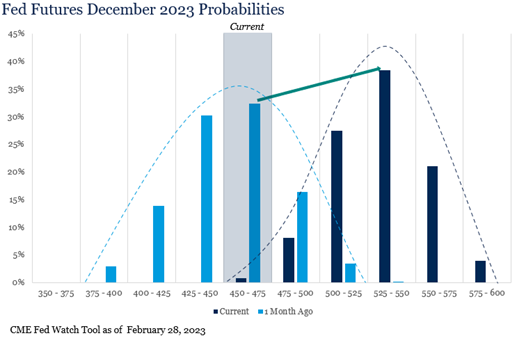

Regardless, markets swallowed these figures whole and shifted their view on the Fed. The graphic above shows probabilities of where the Fed Funds rate will end in December 2023, according to the market. One month ago there was only a 16% probability rates would be higher than 4.5% – 4.75% by year-end. That figure is now 99%. This shift in sentiment has dampened market expectations for a Fed pause / pivot. While perhaps overdone based on the seasonal noise we mentioned, it does speak to the end of rate hikes being near. An unexpected acceleration across several economic fronts shifted expectations 0.50% over 10 months. Last year over the same 10 months from March to December rates rose 4.25%, a 1600% increase. Another 0.50% until December would be an 11% increase. We view rates peaking as a positive step for markets to find their sustainable leg up and we are nearing that point.

Are Earnings the Next Shoe to Drop?

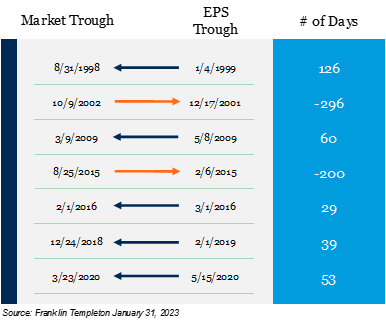

If it is not rates, what is the next shoe for markets? With 94% of companies having reported for the fourth quarter 2022, earnings may sneak away with a positive increase for the year. This is well short of expectations (10%+) and only positive after being bailed out by a very strong year in the energy sector. As of February 24, Q4 2022 earnings declined -4.8%. If that is where earnings finish it will be the worst quarter since Q3 2020 when earnings declined -5.7%, a time when businesses were reeling from shelter-in-place COVID policies**. So does this become the next shoe to drop for markets? It is possible that in the coming quarters disappointing earnings could lead to market volatility as the impact of rates and inflation catch up. However, as we discussed in our 2023 Outlook market volatility should be expected as businesses adjust to non-zero rates and a less accommodative central bank policy. Moreover, even if we could perfectly time the earnings cycle (which no one can), markets tend to move ahead of earnings seeking to anticipate their eventual bottom. Since 1998 markets have led earnings in five of seven drawbacks. In those instances, on average markets have bottomed 61 days prior to earnings. In summary, investors that wait for the all-clear horn on earnings may end up missing the market bottom.

Outlook

We believe continued volatility, moderating inflation, and a market bottom leading to better returns ahead than in 2022 will remain key drivers for the market. The shift in market sentiment around the Fed, while perhaps overdone, speaks to the end is near for rates. This is important in our view for markets to bottom. Earnings may create volatility, but they also create opportunities and are a regular part of the growth and consolidate cycle. Finally, we believe inflation continues to trend in the right direction. Therefore, our view remains that without the power of precision we’ll use the power of preparation to position portfolios for both volatility and opportunity in 2023.

Have you listened to our podcast Wealthy Behavior yet?! It’s a great way to stay up-to-date on today’s markets, economy, and our outlook direct from our CEO, Sammy Azzouz, and CIO, Bob Weisse. Be sure to listen and subscribe so you know when a new episode drops!

*U.S. Bureau of Labor Statistics as of February 28, 2023

**FactSet Earnings Insight as of February 24, 2023